Objective

We now provide proofs of properties presented in Multivariate Regression Basic Concepts.

Proofs (part 1)

Property 1:

B = (XTX)-1XTY

Proof: By univariate regression properties

B = [B1 B2 ⋅⋅⋅ Bm]

= [(XTX)-1XTY1 (XTX)-1XTY2 ⋅⋅⋅ (XTX)-1XTYm]

= (XTX)-1XT[Y1 Y2 ⋅⋅⋅ Ym] = (XTX)-1XTY

Property 2: B minimizes the trace

Tr((Y – XB)T(Y – XB))

Proof: The m × m SSCP matrix S

S = (Y – XB)T(Y – XB)

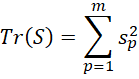

has diagonal terms which are non-negative scalars of the form

![]()

Now

Since the values bjp minimize each term in the above sum, they also minimize the sum.

Property 3:

E[ε] = 0

Proof: This is a consequence of the fact that E[εp] = 0 for all p

Property 4: B is an unbiased estimator of β; i.e. E[B] = β

Proof: By Property 1

B = (XTX)-1XTY

But

Y = Xβ + ε

Thus

B = (XTX)-1XTY = (XTX)–1XT(Xβ+ε)

=(XTX)–1XTXβ + (XTX)–1XTε

= (XTX)–1(XTX)β + (XTX)–1XTε

= β + (XTX)–1XTε

Thus

E[B] = E[β + (XTX)–1XTε] = E[β] + E[(XTX)–1XTε]

= β + (XTX)–1XTE[ε] = β + 0 = β

since E[ε] = 0 by Property 3.

Proofs (part 2)

Property 5:

cov(Bp, Bq) = σpq(XTX)-1

Proof: Using univariate regression properties

Bp = (XTX)-1XTYp= (XTX)–1XT(Xβp + εp)

= (XTX)–1XTXβp + (XTX)–1XTεp = βp + (XTX)–1XTεp

Thus

Bp = βp + (XTX)–1XTεp

and so

Bp – E[Bp] = βp + (XTX)–1XTεp – βp = (XTX)–1XTεp

Similarly

Bq – E[Bq] = (XTX)–1XTεq

Hence

cov(Bp, Bq) = E[((XTX)–1XTεp)((XTX)–1XTεq)T]

= E[(XTX)–1XTεpεqTX(XTX)–1] = (XTX)–1XTE[εpεqT]X(XTX)–1

= (XTX)–1XT(σpqI)X(XTX)–1

The last equality is a result of the fact that E[εpεqT] = E[(εp-E[εp])(εq-E[εq])T] = cov(εp,εq) = σpqI since E[εp] = E[εq] = 0. Finally,

cov(Bp, Bq) = (XTX)–1XT(σpqI)X(XTX)–1

= σpq(XTX)–1(XTX)(XTX)–1 = σpq(XTX)–1

Property 6:

E[Ep] = 0

Proof: Here Ep is the pth column of E = [eip].

E[Ep] = E[Yp–XBp] = E[Yp] – XE[Bp] = E[Yp] – Xβp

The last equality results from the fact that Bp is an unbiased estimator of βp.

But

Yp = Xβp + εp

and so

E[Yp] = E[Xβp + εp] = E[Xβp] + E[εp] = Xβp + 0 = Xβp

Putting everything together, we have

E[Ep] = E[Yp] – Xβp = Xβp – Xβp = 0

Property 7:

cov(Yp, Yq) = σpq

Proof:

cov(Yp, Yq) = (Yp – E[Yp])T(Yq – E[Yq]) = (Yp – Xβp)T(Yq – Xβq)

= εpTεq = cov(εp, εq) = σpq

Trace properties

Before we proceed, we recall some properties of the trace of a square matrix. In particular

Property A:

Trace(Im) = m

Trace(AB) = Trace(BA)

Trace(bA) = bTrace(A)

Trace(A+B) = Trace(A) + Trace(B)

In addition, we prove the following properties.

Property B: For any square matrix A

E[Trace(A)] = Trace(E[A])

Proof: For A = [aij]

E[Trace(A)] = E[∑aii] = ∑ E[aii] = Trace(E[A])

Property C: For any n × n matrix A and n × 1 matrices Y and Z

E[YTAZ] = Trace(A cov(Y,Z)) + E[Y]TA E[Z]

Proof: First note that AZ is also a n × 1 matrix. Thus, as for any covariance

cov(Y, AZ) = E[YTAZ] – E[Y]TE[AZ]

= E[YTAZ] – E[Y]TA E[Z]

Thus

E[YTAZ] = cov(Y, AZ) + E[Y]TA E[Z]

Also

cov(Y, AZ) = E[(Y–E[Y])(AZ–E[AZ]) = E[(Y–E[Y])A(Z–E[Z])

But cov(Y, AZ) is a scalar, and so cov(Y, AZ) = Trace(cov(Y, AZ)). Using the commutivity property of Trace, we obtain

cov(Y, AZ) = Trace(E[(Y–E[Y])A(Z–E[Z])) = Trace(A E[(Y–E[Y])(Z–E[Z]))

= Trace(A E[(Y–E[Y])(Z–E[Z])) = Trace(A cov(Y, Z))

Putting it all together, we get the desired result

E[YTAZ] = cov(Y, AZ) + E[Y]TA E[Z]

= Trace(A cov(Y,Z)) + E[Y]TA E[Z]

Hat matrix properties

We now present some properties of the hat matrix

H = X(XTX)–1XT

Property D: H is symmetric

Proof:

HT = (X(XTX)–1XT)T = X((XTX)–1)TXT = X((XTX)T)-1XT = X(XTX)–1XT = H

Property E: H is idempotent

Proof:

H2 = (X(XTX)–1XT)2 = (X(XTX)–1XT)(X(XTX)–1XT)

= X(XTX)–1(XTX)(XTX)–1XT = X(XTX)–1XT = H

Property F: I – H is symmetric and idempotent

Proof: The result follows from Properties D and E since

(I – H)T = IT – HT = I – H

(I – H)2 = (I – H)(I – H) = I – 2H + H2 = I – 2H + H = I – H

Property G: From Property F, it follows that

(I – H)T(I – H) = I – H

Property H:

Trace(I – H) = dfRes

Proof: Using Property A

Trace(H) = Trace(X(XTX)–1XT) = Trace(XTX(XTX)–1) = Trace(I) = k+1

Trace(I – H) = Trace(I) – Trace(H) = n – Trace(H) = n – k – 1 = dfRes

Proofs (part 3)

Property 8:

E[EpTEq] = σpqdfRes

Proof: Here dfRes = n – k – 1. First we note that

EpTEq = (Yp–XBp)T(Yq–XBq) = (Yp–HYp)T(Yq–HYq)

= ((I–H)Yp)T((I–H)Yq) = YpT(I–H)T(I–H)Yq = YpT(I–H)Yq

The last equality follows from Property G. Thus

EpTEq = YpT(I–H)Yq

By Property C

E[YpT(I–H)Yq] = Trace((I–H) cov(Yp, Yq)) + E[Yp]T(I–H)E[Yq]

By Properties 7 and A,

Trace((I–H) cov(Yp, Yq)) = Trace(I–H) ⋅ Trace (cov(Yp, Yq))

= dfRes ⋅ Trace (σpq) = σpq dfRes

Finally, note that

E[YpT](I–H)E[Yq] = (Xβp)T(I–X(XTX)–1XT)(Xβq)

=(Xβp)T(Xβq) – βpTXTX(XTX)–1XTXβq = (Xβp)T(Xβq) – βpTXTXβq = 0

Putting it all together, we have

E[EpTEq]= E[YpT(I–H)Yq] = Trace((I-H) cov(Yp, Yq)) + E[Yp]T(I–H)E[Yq]

= σpqdfRes + 0 = σpqdfRes

Property 9: SSE/dfRes is an unbiased estimate for Σ; i.e. E[SSE] = E[ETE] = dfResΣ

Proof: This is a consequence of Property 8.

Property 10:

cov(Bp, Eq) = 0 cov(B, E) = 0

Proof: The proof of the first assertion is similar to that for Property 8. The second assertion follows from the first.

References

Johnson, R. A., Wichern, D. W. (2007) Applied multivariate statistical analysis. 6th Ed. Pearson

https://mathematics.foi.hr/Applied%20Multivariate%20Statistical%20Analysis%20by%20Johnson%20and%20Wichern.pdf

Rencher, A.C., Christensen, W. F. (2012) Methods of multivariate analysis (3nd Ed). Wiley

Stack Exchange (2011) How to prove that the expression ….

https://math.stackexchange.com/questions/93994/how-to-prove-that-the-expression-ezaz-for-a-random-vector-z-is