Moving Average Basic Concepts

The following are proofs of properties found in Moving Averages Basic Concepts

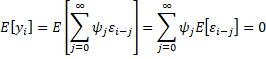

Property 1: The mean of an MA(q) process is μ.

Proof:

![]()

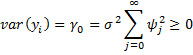

Property 2: The variance of an MA(q) process is

![]()

Proof:

![]()

Property 3: The autocorrelation function of an MA(1) process is

![]() Proof:

Proof:![]()

![]() When h = 1

When h = 1![]() since E[εi-1] = 0. When h > 1

since E[εi-1] = 0. When h > 1

![]()

Thus for h = 1, by Property 2

![]()

and for h > 1

![]()

Property 4: The autocorrelation function of an MA(2) process is

![]()

Proof:

![]()

![]()

![]()

Thus, when h = 1

![]()

and when h = 2

![]()

and when h > 2

![]()

It now follows that for h = 1, by Property 2

![]()

and for h = 2

![]()

and for h > 2

![]()

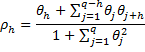

Property 5: The autocorrelation function of an MA(q) process is

for h ≤ q and ρh = 0 for h > q.

Proof: As in the proof of Property 3 of Autoregressive Processes, it is sufficient to prove the property in the case where the mean = 0 (and so the constant term is zero). Since E[εiεi] = σ2 and E[εiεi-j] = 0 when j > 1, it follows that

![]()

for h ≤ q and cov(yi, yi-h) = 0 if h > q.

By Property 2 it now follows that

for h ≤ q and ρh = 0 for h > q.

Infinite Moving Average Processes

The following is a proof of Property 4 in Infinite Moving Average Processes.

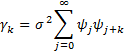

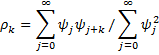

Property 4: The following are true for any MA(∞) process

![]()

Proof: The assumption that the infinite sum of the absolute values of the ψi terms is finite is needed to show that all the infinite series listed below converge. As usual, it is sufficient to demonstrate the above properties in the case where the mean is 0.

since E[εi-jεi+k-h] = σ2 if h = j+k and zero otherwise.

The other two properties follow from this last one.

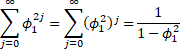

Observation: Property 4 can be used to provide an alternative proof of various properties of AR(p) processes. For example, for an AR(1) process we have seen that ψj = φ1j, and so

This last equality results from the fact that |φ1| < 1, and so φ12 < 1, in which case we have a geometric series that converges as follows:

See Geometric Series for a proof that the geometric series converges.

References

Greene, W. H. (2002) Econometric analysis. 5th Ed. Prentice-Hall

https://www.ctanujit.org/uploads/2/5/3/9/25393293/_econometric_analysis_by_greence.pdf

Gujarati, D. & Porter, D. (2009) Basic econometrics. 5th Ed. McGraw Hill

http://www.uop.edu.pk/ocontents/gujarati_book.pdf

Hamilton, J. D. (1994) Time series analysis. Princeton University Press

https://press.princeton.edu/books/hardcover/9780691042893/time-series-analysis

Wooldridge, J. M. (2009) Introductory econometrics, a modern approach. 5th Ed. South-Western, Cegage Learning

https://cbpbu.ac.in/userfiles/file/2020/STUDY_MAT/ECO/2.pdf

Wei, W. (2006) Time series analysis: univariate and multivariate methods, 2nd edition. Pearson Addison Wesley https://www.researchgate.net/publication/236651810_Time_Series_Analysis_Univariate_and_Multivariate_Methods_2nd_edition_2006