Basic Concepts

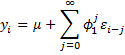

An infinite-order moving average process, denoted MA(∞), takes the form

where the following infinite sum is finite (i.e. converges to a real value)

and

εi ∼ N(0, σ2) cov(εi, εj) = 0 if i ≠ j

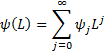

We can also express an MA(∞) process as

where it is assumed that ψ0 = 1.

Observation: That

AR(1) Process

Example 1

Show that the AR(1) process from Example 1 of Autoregressive Processes Basic Concepts can be represented by an MA(∞) process.

![]()

By Property 1 of Autoregressive Processes Basic Concepts

![]()

Now define![]()

Then the original AR(1) process can be transformed into the process

![]()

which is![]()

But then![]()

and so![]()

which means that![]()

Similarly![]()

which results in

![]()

Continuing in this way, we get

and so

which is the desired MA(∞) process.

Property 1

Any stationary AR(1) process can be expressed as an MA(∞) process. In fact

![]()

Proof: Using the same approach as in Example 1, we find that the AR(1) process

![]()

can be expressed as

where![]()

Since the original process is a stationary AR(1), |φ1| < 1 and the εi have the desired properties.

Observation

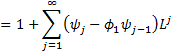

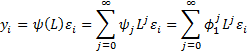

Another way to see this is to use the lag operator, namely that an AR(1) process (with zero mean) can be expressed as

![]()

where![]()

as well as![]()

where

Substituting the first equation inside the second, we get

![]()

i.e.

Here we recall that φ0 = 1. Equating the coefficients, we see that for all j > 0

Here we recall that φ0 = 1. Equating the coefficients, we see that for all j > 0

![]()

Thus

![]()

![]() etc.

etc.

and so we that![]()

It follows that

We also observed above that![]()

and so ψ(L) is the inverse of φ(L)![]()

AR(p) and MA(∞) equivalence

Property 2: Any stationary AR(p) process can be expressed as an MA(∞) process.

Proof: The proof is similar to that of Property 1.

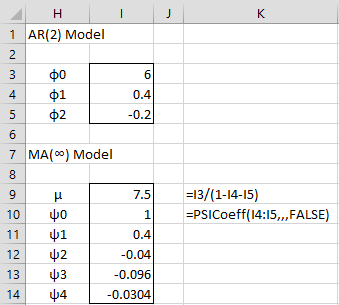

AR(2) Example

Example 2: Show that the following AR(2) process can be represented by an MA(∞) process.

![]()

By Property 1 of Autoregressive Processes Basic Concepts, the mean is

![]()

Now define![]()

Then the original AR(2) process can be transformed into the process

![]() But then

But then![]()

![]()

![]() and so

and so

![]()

![]()

![]()

etc. Thus the first few terms of the MA(∞) process are

![]()

Key Properties

Property 3 (Wold’s Decomposition Theorem): Any stationary process can be represented as an MA(∞) process

Property 4: The following are true for any MA(∞) process

![]()

Proof: See Moving Average Proofs

Worksheet Function

Real Statistics Function: The Real Statistics Resource Pack provides the following array function where R1 is a column range consisting of phi coefficients and R2 is a column range consisting of theta coefficients.

PSICoeff(R1, R2, k, rev): returns a k × 1 range containing the first k psi coefficients (starting with ψ0 = 1) for the ARMA model with the coefficients in R1 and R2.

If k is omitted (default) then k is set equal to the number of rows in the highlighted range. If rev = TRUE (default), then the phi and theta coefficients are listed in reverse order φp, φp-1, …, φ1 and order θq, θq-1, …, θ1.

Since both phi and theta coefficients can be present, this function can also handle ARMA processes as described in ARMA Processes.

We can use the PSICoeff function to find the psi coefficients for Example 2 as shown in range I10:I14 of Figure 1.

Figure 1 – Convert AR(2) model into an MA(∞) model

Examples Workbook

Click here to download the Excel workbook with the examples described on this webpage.

References

Greene, W. H. (2002) Econometric analysis. 5th Ed. Prentice-Hall

https://www.ctanujit.org/uploads/2/5/3/9/25393293/_econometric_analysis_by_greence.pdf

Gujarati, D. & Porter, D. (2009) Basic econometrics. 5th Ed. McGraw Hill

http://www.uop.edu.pk/ocontents/gujarati_book.pdf

Hamilton, J. D. (1994) Time series analysis. Princeton University Press

https://press.princeton.edu/books/hardcover/9780691042893/time-series-analysis

Wooldridge, J. M. (2009) Introductory econometrics, a modern approach. 5th Ed. South-Western, Cegage Learning

https://cbpbu.ac.in/userfiles/file/2020/STUDY_MAT/ECO/2.pdf

Wei, W. (2006) Time series analysis: univariate and multivariate methods, 2nd edition. Pearson Addison Wesley https://www.researchgate.net/publication/236651810_Time_Series_Analysis_Univariate_and_Multivariate_Methods_2nd_edition_2006

How can I calculate the covariance and autocorrelation of infinite moving average process

Ligawa,

Sorry, but I don’t know the answer to your question.

Charles

if y(t)=e(t)+5 e(t-1)+10e(t-2), e(t)~N(0,16), what’s the inverse of that MA model?

Hello Assma,

See the following webpage about the inverse of an MA(q) model.

https://www.real-statistics.com/time-series-analysis/moving-average-processes/invertibility-ma-processes/

Charles

Very resourceful and useful to me. Thank you