Basic Concepts

The additive Holt-Winters model is identical to the multiplicative model, except that seasonality is considered to be additive. This means that the forecasted value for each data element is the sum of the baseline, trend, and seasonality components. The sum of the seasonality components for c consecutive periods of time is approximately 1.

The recursive approach to the additive model is

![]()

![]()

![]()

where 0 ≤ α ≤ 1, 0 ≤ β ≤ 1 and 0 ≤ γ ≤ 1.

The predictions for the data elements yi is given by

![]()

For forecasts at future times, we use the form

![]() where h′ =INT((h–1)/c)+1.

where h′ =INT((h–1)/c)+1.

Alternative Form

An alternative version of the seasonality term is:

![]()

Based on this version of the seasonality term, we have the following alternative form of the recursive equations:

![]()

![]()

![]()

![]()

Example

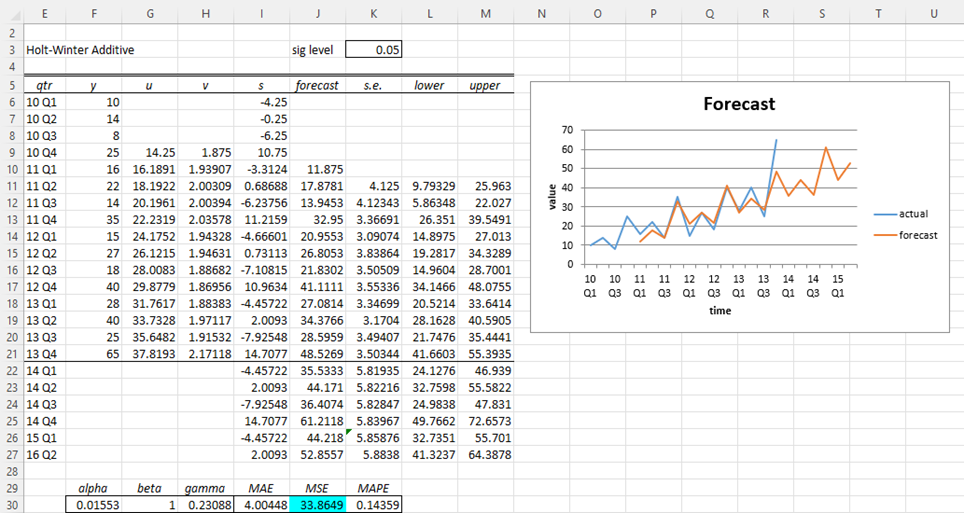

Example 1: Forecast the y values for 2014 (i.e. the next four quarters) using Holt-Winter’s additive method based on the data in range E4:F19 of Figure 1 using the alpha, beta, and gamma values that minimize the MSE statistic.

This is the same problem as Example 2 in Holt-Winters’ Multiplicative Method, except now we need to apply the additive method.

The result is shown in Figure 1.

Figure 1 – Holt-Winters’ Additive Forecast

You can get similar results by using the Real Statistics Basic Forecasting data analysis tool, as described in Real Statistics Basic Forecasting Tool. This data analysis tool also displays the standard errors and confidence intervals of the forecasts.

Standard errors and prediction intervals

Click here for an example of how to obtain the standard errors and confidence intervals for the forecast obtained via the Holt-Winters additive method.

Examples Workbook

Click here to download the Excel workbook with the examples described on this webpage.

Reference

Hyndman, R. J., and Athanasopoulos, G. (2021) Holt-Winters’ seasonal method. Forecasting: principals and practice, 3rd Ed.

https://otexts.com/fpp3/holt-winters.html

Charles, I noticed the time period lag cited in the reference text also: https://otexts.com/fpp3/taxonomy.html

Any explanation why? I am trying to include a damping factor in the model I am building

Hello Spencer,

What I am calling gamma γ is called gamma γ* on the following webpage

https://otexts.com/fpp3/holt-winters.html

In this case, the reference is to u_i.

Charles

Charles, I noticed u i-1 in the reference text also: https://otexts.com/fpp3/taxonomy.html Any explanation why? I am trying to include a damping factor in the model I am building

Spencer,

Are you referring to the damping factor described at https://otexts.com/fpp3/holt-winters.html ?

Real Statistics doesn’t support this as yet, but I will consider adding it.

Charles

Thank you Charles! Also, great website — appreciate your contribution to society 🙂

Hello Charles Sir,

In the above Holt Winter Additive Model the formula for “s” is mentioned as

s = gamma * { y(i) – u (i-1)} + {1-gamma}* s(i-c)

but in the XRealStats tool the embedded formula uses value of “u” instead of “u-1”

Request you to please check and clarify

Hello Prashant,

It should be u_i. I have just made the change on the webpage.

Thank you very much for catching this error.

Charles