Basic Concept

We now define the lag function as

![]()

Here, we assume that

![]()

for any constant c and any variables x and z. We also use the following notation for any variable z and non-negative integer n.

AR(p) process

AR(p) process

We can express the AR(p) process

![]()

using the lag function notation as

![]()

or even![]()

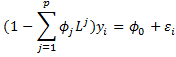

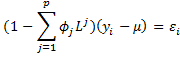

Here, 1 is the identity function and we use the notation (f+g)x to mean f(x) + g(x) for any functions f and g. Using this notation, we can also express an AR(p) process by

By Property 1 of Autoregressive Process Basic Concepts, this is equivalent to

![]()

or

Note that

![]()

is a pth degree polynomial which is equivalent to the characteristic polynomial of the AR(p) process, as described in Characteristic Equation for Autoregressive Processes. This polynomial can be factored (by the Fundamental Theorem of Algebra) as follows

![]()

where the values r1, r2, …, rp are the characteristic roots of the AR(p) process.

Based on the vector φ = [φ1, …, φp] of coefficients, we can define the operator φ(L)

![]()

and so an autoregression process can be expressed succinctly as

![]()

Final Note

The lag function is also called the (back) shift operator, and so sometimes the symbol B is used in place of L.

Links

References

Greene, W. H. (2002) Econometric analysis. 5th Ed. Prentice-Hall

https://www.ctanujit.org/uploads/2/5/3/9/25393293/_econometric_analysis_by_greence.pdf

Gujarati, D. & Porter, D. (2009) Basic econometrics. 5th Ed. McGraw Hill

http://www.uop.edu.pk/ocontents/gujarati_book.pdf

Hamilton, J. D. (1994) Time series analysis. Princeton University Press

https://press.princeton.edu/books/hardcover/9780691042893/time-series-analysis

Wooldridge, J. M. (2009) Introductory econometrics, a modern approach. 5th Ed. South-Western, Cegage Learning

https://cbpbu.ac.in/userfiles/file/2020/STUDY_MAT/ECO/2.pdf