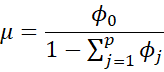

Basic Properties

Property 1: The mean of the yi in a stationary AR(p) process is

Proof: Since the process is stationary, for any k, E[yi] = E[yi-k], a value which we will denote μ. Since E[εi] = 0, E[φ0] = φ0 and

![]()

it follows that

![]()

Solving for μ yields the desired result.

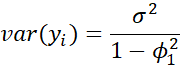

Property 2: The variance of the yi in a stationary AR(1) process is

Proof: Since the yi and εi are independent, by basic properties of variance, it follows that

![]()

![]()

Since the process is stationary, var(yi) = var(yi-1), and so

![]()

Solving for var(yi) yields the desired result.

Property 3: The lag h autocorrelation in a stationary AR(1) process is

![]()

Proof: First note that for any constant a, cov(a+x, a+y) = cov(x,y). Thus, cov(yi,yj) has the same value even if we assume that φ0 = 0, and similarly for var(yi) = cov(yi,yi). Thus, it suffices to prove the property when φ0 = 0. In this case, by Property 1, μ = 0, and so cov(yi,yj) = E[yiyj].

Thus

![]()

since by the stationary property, E[yi-1,yi-k] = γi-1. Now, by induction on k, it is easy to see that

![]()

Hence![]() Yule-Walker equations

Yule-Walker equations

Property 4 : For any stationary AR(p) process, we can calculate the autocovariance at lag k > 0 by

![]()

Similarly, the autocorrelation at lag k > 0 can be calculated as

![]()

Proof: As usual, we can assume that the mean is zero (and so φ0 = 0). Thus, we are dealing with the process

![]()

Thus

The second form of the property follows by dividing both sides of the equation by γ0.

Proof of Property 7

Property 7: The variance of the yi in a stationary AR(2) process is

![]()

Proof:

![]()

![]()

By the stationary property

![]()

and so

![]()

But by Property 4,

![]()

and so

The result follows by expanding the terms in the denominator and seeing that these are equal to the expansion of the denominator in the statement of the property.

Links

↑ Autoregressive processes basic concepts

References

Alonso, A. M., Garcia-Martos, C. (2012) Time series analysis: autoregressive, MA and ARMA processes

https://www.academia.edu/35659911/Time_Series_Analysis_Autoregressive_MA_and_ARMA_processes

Greene, W. H. (2002) Econometric analysis. 5th Ed. Prentice-Hall

https://www.ctanujit.org/uploads/2/5/3/9/25393293/_econometric_analysis_by_greence.pdf

I love that you have proofs here, and I love the format. This has been useful for my final exam study for my time-series course. Many textbooks only provide proofs for the general AR(p) case, which makes it more difficult to follow, and frustrating when I know how to use the formula.

Dear Charles, In Property 2 proof, line 6. It mentioned the below.

“Since the process is stationary, yi = yi-1, and so”. Would you please elaborate how true this statement is ? Shouldn’t the statement states that, Since the process is stationary, var(yi)=var(yi-1), and so ?

Hello Ranil,

Yes, of course you are correct. Thanks for identifying this error. I have now corrected the webpage.

Thanks for bringing this error to my attention.

Charles

You are welcome Charles.

Dear Sir,

By when will you be able to post all the proofs…….

Pankaj,

After I finish with Release 5.3 of the Real Statistics software.

Charles

please post the proof.

Pankaj,

Sorry, but it looks like I forgot to add this webpage. I am now finishing up the testing for the next release of the Real Statistics software (rel 5.3). When I have finished this, I will add the missing proofs.

Charles