The one-sample Kolmogorov-Smirnov test is used to test whether a sample comes from a specific distribution. We can use this procedure to determine whether a sample comes from a population that is normally distributed. See Kolmogorov-Smirnov Test for Normality.

We now show how to modify the procedure to test whether a sample comes from an exponential distribution. Tests for other distributions are similar.

Example

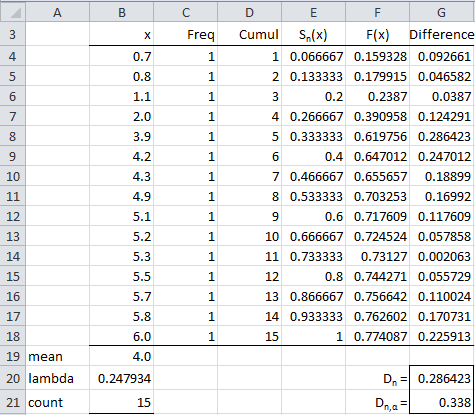

Example 1: Determine whether the sample data in range B4:B18 of Figure 1 is distributed significantly different from an exponential distribution.

Figure 1 – Kolmogorov-Smirnov test for exponential distribution

The result is shown in Figure 1. This figure is very similar to Figure 3 of Kolmogorov-Smirnov Test for Normality. Assuming the null hypothesis holds, and the data follows an exponential distribution, the data in column F would contain the cumulative distribution values F(x) for every x in column B.

We use the Excel function EXPON.DIST to calculate the exponential distribution valued F(x) in column F. E.g. the formula in cell F4 is =EXPON.DIST(B4,$B$20,TRUE). Here, B4 contains the x value (0.7 in this case), and B20 contains the value of lambda (λ) in the definition of the exponential distribution (Definition 1 of Exponential Distribution). As we can see from Figure 1 of Exponential Distribution, λ is simply the reciprocal of the population mean. As usual, we use the sample mean as an estimate of the population mean, and so the value in B20, which contains the formula =1/B19 where B19 contains the sample mean, is used as an estimate of λ.

All the other formulas are the same as described in Kolmogorov-Smirnov Test for Normality where the Kolmogorov-Smirnov test is used to test that the data set follows a normal distribution.

Results

We see that the test statistic D is .286423 (cell G20, which contains the formula =MAX(G4:G18)). We also see that D is less than the critical value of 0.338 (cell G21, which contains the formula =KSCRIT(B21,0.05), i.e. the value for n = 15 and α = .05 in the Kolmogorov-Smirnov Table). Since D < Dcrit, we conclude that there is no significant difference between the data and data coming from an exponential distribution (with λ = 0.247934).

We can compute an approximate p-value using the formula

KSPROB(G20,B21) = .141851

Caution

The one-sample KS Test works best when the parameters of the distribution being fit are known. When the parameters are estimated from the sample, the critical values need to be reduced. This is demonstrated in Lilliefors Test where a different table of critical values is used for fitting data to a normal distribution. If the distribution parameters need to be estimated from the sample, then you can use the One-sample Anderson-Darling Test for goodness-of-fit testing.

Examples Workbook

Click here to download the Excel workbook with the examples described on this webpage.

Links

References

National Institute of Standards and Technology NIST (2021) Kolmogorov-Smirnov goodness-of-fit test

https://www.itl.nist.gov/div898/handbook/eda/section3/eda35g.htm

Wikipedia (2012) Kolmogorov-Smirnov test

https://en.wikipedia.org/wiki/Kolmogorov%E2%80%93Smirnov_test

This is really helpful. I am trying to find the critical value for one sample KS test (testing titled Laplace distribution fit) for annual change using monthly data so there is 11 month overlapping data involved. Is it possible to adjustment to the below critical value formula for 11 month overlapping data? my total data points are around 1000 monthly data points. (around 83 years)

D(n,alpha) = D(alpha)/(sqrt(n)+0.12+0.11/sqrt(n))

alpha=0.05, n=1000

Hello Manish,

If you know the parameter values of the Laplace distribution, then you can use the KS test as described on the Real Statistics website and software. If the parameter values are not known and need to be estimated from the data (the usual situation), then, unfortunately, the KS test for this distribution is not yet supported by Real Statistics.

You can use the approach described at

Puig, P. and Stephens, M. A. (2000) Tests of Fit for the Laplace Distribution, With Applications

https://www.researchgate.net/publication/240278042

I plan to add the Anderson-Darling version of this test to Real Statistics. In general, the Anderson-Darling test is better than the KS test.

Charles

Hello, Charles.

Is it possible to use the Kolmogorov-Smirnov single-sample test to check whether a sample is being sampled from Benford’s distribution?The critical values of the Kolmogorov-Smirnov test statistics are taken from https://en.wikipedia.org/wiki/Benford%27s_law

For α 0.10 1.012; for α 0.05 1.148; for α 0.01 1.420?

Thank you in advance for the answer!

Hello Konstantin,

Yes, perform the test in the usual way, except that you should use these critical values instead of the usual values from the critical value table.

Charles

Charles, Thank you!

Hello Konstantin,

I plan to add goodness-of-fit tests for Benford’s distribution (using chi-square, KS, and AD) to the next release of the Real Statistics software.

Charles

Hello Charles,

fan of your work. You’ve said for other distributions we follow the same procedure. But I’m stuck with Pareto_Dist. I need to to KS test for a Pareto fit (one data sample vs. theoretical pareto distribution). Can you post an example for Pareto distribution fitting as well?

Thanks in advance,

Hello Anil,

Suppose that you are testing the data in range B4:B18 of Figure 1 for a fit with a Pareto distribution with parameters alpha = 2.4 and mn = 1.9. We now place these two parameters in cells B20 and C20. We also need to modify the formulas in column F. E.g. the formula in cell F4 now becomes =PARETO_DIST(B4,B$20,C$20,TRUE).

This is the process to use if you already know the values of the two parameters. If not, then you need to estimate these parameters from the data. Two approaches are described on the Real Statistics website: method of moments and maximum likelihood estimate (MLE). These are described at

https://www.real-statistics.com/distribution-fitting/method-of-moments/method-of-moments-pareto-distribution/

https://www.real-statistics.com/distribution-fitting/distribution-fitting-via-maximum-likelihood/fitting-pareto-parameters-via-mle/

Note that the KS procedure is not as accurate when you estimate the parameters from the data. This is why for the normal distribution the usual KS method is replaced by a modified KS process (called Lilliefors method) when the normal parameters are estimated from the data.

Charles

wealth_2006_100 Freq Cumulative Sn(X) F(X) Difference

1800 1 1 0,0100 0,9332 0,9232

1506 1 2 0,0200 0,9085 0,8885

1501 1 3 0,0300 0,9079 0,8779

1474 1 4 0,0400 0,9049 0,8649

1454 1 5 0,0500 0,9026 0,8526

1395 1 6 0,0600 0,8952 0,8352

1380 1 7 0,0700 0,8932 0,8232

1360 1 8 0,0800 0,8904 0,8104

1310 1 9 0,0900 0,8829 0,7929

1250 1 10 0,1000 0,8727 0,7727

1228 1 11 0,1100 0,8687 0,7587

1200 1 12 0,1200 0,8632 0,7432

1150 1 13 0,1300 0,8525 0,7225

1145 1 14 0,1400 0,8513 0,7113

1100 1 15 0,1500 0,8404 0,6904

1100 1 16 0,1600 0,8404 0,6804

1100 1 17 0,1700 0,8404 0,6704

1075 1 18 0,1800 0,8338 0,6538

1060 1 19 0,1900 0,8296 0,6396

1050 1 20 0,2000 0,8267 0,6267

975 1 21 0,2100 0,8024 0,5924

950 1 22 0,2200 0,7931 0,5731

940 1 23 0,2300 0,7892 0,5592

925 1 24 0,2400 0,7831 0,5431

925 1 25 0,2500 0,7831 0,5331

910 1 26 0,2600 0,7768 0,5168

900 1 27 0,2700 0,7724 0,5024

900 1 28 0,2800 0,7724 0,4924

900 1 29 0,2900 0,7724 0,4824

875 1 30 0,3000 0,7607 0,4607

870 1 31 0,3100 0,7583 0,4483

850 1 32 0,3200 0,7481 0,4281

850 1 33 0,3300 0,7481 0,4181

820 1 34 0,3400 0,7316 0,3916

803 1 35 0,3500 0,7214 0,3714

770 1 36 0,3600 0,7000 0,3400

750 1 37 0,3700 0,6857 0,3157

750 1 38 0,3800 0,6857 0,3057

750 1 39 0,3900 0,6857 0,2957

725 1 40 0,4000 0,6662 0,2662

710 1 41 0,4100 0,6537 0,2437

700 1 42 0,4200 0,6448 0,2248

685 1 43 0,4300 0,6310 0,2010

685 1 44 0,4400 0,6310 0,1910

685 1 45 0,4500 0,6310 0,1810

675 1 46 0,4600 0,6212 0,1612

665 1 47 0,4700 0,6111 0,1411

660 1 48 0,4800 0,6059 0,1259

650 1 49 0,4900 0,5951 0,1051

650 1 50 0,5000 0,5951 0,0951

650 1 51 0,5100 0,5951 0,0851

650 1 52 0,5200 0,5951 0,0751

650 1 53 0,5300 0,5951 0,0651

640 1 54 0,5400 0,5838 0,0438

630 1 55 0,5500 0,5720 0,0220

620 1 56 0,5600 0,5598 -0,0002

620 1 57 0,5700 0,5598 -0,0102

615 1 58 0,5800 0,5534 -0,0266

605 1 59 0,5900 0,5403 -0,0497

600 1 60 0,6000 0,5335 -0,0665

590 1 61 0,6100 0,5194 -0,0906

575 1 62 0,6200 0,4970 -0,1230

550 1 63 0,6300 0,4558 -0,1742

550 1 64 0,6400 0,4558 -0,1842

550 1 65 0,6500 0,4558 -0,1942

545 1 66 0,6600 0,4469 -0,2131

525 1 67 0,6700 0,4091 -0,2609

520 1 68 0,6800 0,3990 -0,2810

510 1 69 0,6900 0,3780 -0,3120

500 1 70 0,7000 0,3558 -0,3442

500 1 71 0,7100 0,3558 -0,3542

500 1 72 0,7200 0,3558 -0,3642

500 1 73 0,7300 0,3558 -0,3742

500 1 74 0,7400 0,3558 -0,3842

485 1 75 0,7500 0,3201 -0,4299

480 1 76 0,7600 0,3075 -0,4525

480 1 77 0,7700 0,3075 -0,4625

465 1 78 0,7800 0,2675 -0,5125

460 1 79 0,7900 0,2533 -0,5367

455 1 80 0,8000 0,2388 -0,5612

450 1 81 0,8100 0,2237 -0,5863

450 1 82 0,8200 0,2237 -0,5963

450 1 83 0,8300 0,2237 -0,6063

450 1 84 0,8400 0,2237 -0,6163

450 1 85 0,8500 0,2237 -0,6263

436 1 86 0,8600 0,1791 -0,6809

435 1 87 0,8700 0,1757 -0,6943

435 1 88 0,8800 0,1757 -0,7043

435 1 89 0,8900 0,1757 -0,7143

435 1 90 0,9000 0,1757 -0,7243

425 1 91 0,9100 0,1411 -0,7689

420 1 92 0,9200 0,1229 -0,7971

400 1 93 0,9300 0,0438 -0,8862

400 1 94 0,9400 0,0438 -0,8962

400 1 95 0,9500 0,0438 -0,9062

400 1 96 0,9600 0,0438 -0,9162

400 1 97 0,9700 0,0438 -0,9262

400 1 98 0,9800 0,0438 -0,9362

400 1 99 0,9900 0,0438 -0,9462

390 1 100 1,0000 0,0000 -1,0000

mean 745 D= 0,9232

Dcrit= 0,1358

count 100

alpha 1,7698

This is what I’ve done. 390 is the minimum and estimated (from the data, by MLE, on a different sheet) alpha is 1,7697

The differences are too large though… Could it be because I need to invert F(X) order maybe?! Because Sn(x) increasing (obviously, cumulatively adding up to 1) but F(X) is decreasing to zero, hence differences go from very high positive to very high negative -1, always greater than the D_critical for KS. 🤔

Can you send me an Excel spreadsheet with this analysis?

Charles

Hi Charles,

I was trying to understand the Kolmogorov Smirnov test and came across your site and it really helps in understanding the concept. It would be great if you can explain, does KS test is sensitive to data normalization.

For example, if my dataset is lognormal then ln(x) transformed it to Normal.

Now, after this transformation, if the mean & std dev of my transformed data is not equal to (0,1) then will it make any difference?

I’m asking this question because I’m getting totally different p-values:

1. When the transformed data is standard scaled i.e. (mean, std dev) == (0,1)

In this case, the p-value is coming very low

2. Transformed data is not scaled i.e. (mean, std dev) != (0,1)

In this case, the p-value is coming high

Just a note here, I’m using python in place of excel and trying to understand whether it is one of the KS test concepts or the implementation difference.

Rajesh,

Data has a lognormal distribution when the natural log, ln x, of the data is normally distributed, but this does not mean that the result is standard normal with mean zero and standard deviation one.

If you email me an Excel file with your data and results illustrating points #1 and #2, I will try to figure out what is going on.

Charles

Thank you for sharing this information. it really helps. I really appreciate if you can answer these questions too:

1) if we are testing data against lognormal dist., why do you suggest to transform it to normal? there are formulas in Matlab for exp. that computes the theoretical CDF of X based on the parameters of the samples. I mean there isn’t any difference if we compare the empirical CDF with the lognormal CDF of the original data. is there?

2) Also, if you can explain the difference between two-sided and on0sided test of KS, I really appreciate it.

Hello Arash,

I am pleased that you find the Real Statistics website helpful.

1) You can certainly perform the KS test directly on lognormal data. If you estimate the mu and sigma parameters from the data, then you need to make sure that you use an equivalent of the Lillifours critical values. I didn’t provide all the various one-sample KS tests since the Anderson-Darling one sample test is a much better test.

2) See https://stats.stackexchange.com/questions/107668/does-it-make-sense-to-perform-a-one-tailed-kolmogorov-smirnov-test

Charles

Hi Charles,

If I want to test whether my set of data follows log-normal distribution, what is the best method to use? can I use KS method?

Thank you.

Hi Jessica,

Yes, you can use a KS test. If you are estimating the mu and sigma values from the sample data, then you should use the Lilliefors version of the KS test since the results will be more accurate. See Lilliefors Test

Since you are testing for log-normality you need to first transform your data via LN(x) (x is log-normal if ln(x) is normal).

A better test for log-normality is the one-sample Anderson-Darling test. See one-sample Anderson-Darling Test

Charles

Thank you for sharing your knowledge. If you do not mind, I have a question, can I use this method for two -sample KS test of similarity that have the same number of frequency (1). what is you suggestion if I change both function into exponential distribution as you did in the above example and find D and D crt and make decision whether the a pair of distributed values are similar or not?

Gebre,

I suggest that you try to do this and see what happens.

Charles

Charles,

Do you have a reference for hard-copy tables of the Kolmogorov-Smirnov One-Sample test for a Uniform distribution, N >50 ?

No Stephen, I don’t have such a reference.

Charles

hi Charles…

I would like to know the reference that you used to decide the score of Kolmogrov Smirnov for the level of significance (.05)

Wildan,

Are you asking for the reference to Kolmogorov-Smirnov table of critical values? If so, if you google you should find numerous references to the table of critical values.

Charles

I really not aware how to calculate s(x)

As described on the referenced webpage, please see the following webpage

Kolmogorov-Smirnov Test for Normality

Charles

Hi Charles,

I am wondering if a variable has good normality in KS test, can I use anova after?

Many thanks.

Tian

Tian,

In general I would recommend the Shapiro-Wilk test for normality rather than the KS test. If you do use the KS test then make sure that you use the Lilliefors version of the test if the mean and standard deviation are estimated from the sample.

If the test for normality holds then you can use Anova provided that the other assumptions hold (especially homogeneity of variances).

Charles

Hi sir

why can i only need to consider one side of the difference?

I mean only

abs(cumul/count-F(x))———–1

but not

abs(F(x)-(cumul-1)/n)————2

it makes more sense to me if D_n=max{1,2},since the step function is discontinuous at x

thx!

Leung,

Sorry, but I don’t quite understand what the other side of the difference is. In any case, the KS test is the one described. Perhaps there are other possible tests along the lines that you are describing.

Charles

Hi Charles, I guess what Leung tried to highlight is that Kolmogorov test statistic D_n considers sup_x|Fn(x)-F(x)|, which for computation purposes is translated into max_i{|F(x_i)-(i-1)/n|,|i/n-F(x_i)|}.

If the question simply tells you to test whether 2 variables follow a normal distribution, should I use the One-Sample K-S Test or rather consider the p-value of the Kolmogorov-Smirnov Test from the Tests of Normality (which in SPSS is given with the Lilliefors Significance Correction)?

Thanks in advance!

Steve,

In general I would use the Shapiro-Wilk test. It is more accurate.

If you are testing for a normal distribution with a specified mean and standard deviation then you could use the one-sample KS test. If you don’t know the population mean and standard deviation (and will estimate these from the sample), then you should use the Lilliefors version of the test.

Charles

Hi, Charles

I’m confuse how to calculate the value of Sn(x)?

Christian,

Sn(x) is explained on the following webpage

Charles

In your page ‘Kolmogorov-Smirnov Test for Normality’, the Sn(x)=k/n, if x(k) <= x < x(k+1). So what is the value of 'k'?

Hi Charles,

Regarding p-value, what is the difference between your formula KSPROB(D-statistic, Sample size) and KSDIST(D-statistic,Sample Size). On this page, the p-value is calculated using KSPROB. In the normality case, you used KSDIST. What is the difference. Thanks.

Jacky,

They both represent approximate values for the p-value. KSPROB(x,n) = the p-value estimated using the table of critical values. E.g., KSPROB(.24,30) = .05 because the critical value for alpha = .05 and n = 30 is .24. For values not in the table of critical values a harmonic interpolation is made: e.g. KSPROB(.23,30) = .0667; here .22 and .24 are in the table of critical values but .23 is not so a value between the two critical values is used.

The KSDIST(x,n) function uses a different approach, namely it calculates the p-value using an approximate Kolmogorov distribution function.

Neither value is perfect (nor are they always equal).

Charles

Don’t we able to one sample test on k-s test? like gamma distribution?

Sorry, but I don’t understand your question.

Charles

Hi

My research have two verible

avergae performance Cash F. (Before)….1

average performance Cash F. (After)…..2

Can I use KS to know if there are differnt to use before and After

You would typically use a paired t test or Wilcoxon signed ranks test for this sort of problem. A one sample KS test is typically used to see whether a sample fits a particular distribution.

Charles

Hi, sir

Since the null hypothesis for KS is that a set of data do not display a normal distribution, which means they are significantly different from each other.

If I just want to find out whether several figures, for instance, 1.1, 1.2, 1.4, 1.5, are significantly different from each other, only an one-sample KS test is OK?

Stacey,

A one-sample KS test can be used to determine whether a sample (such as the one you have listed) is normally distributed, i.e. that the sample is not significantly different from a normal distribution (not that the numbers in the sample are significantly different from each other). If you have the mean and standard deviation of the normal distribution, then you can use the KS test directly. If instead you are estimating the mean and standard deviation from the sample data, then you should use the Lilliefors version of the KS test, as described on the webpage

Lilliefors Test for Normality.

Charles

Thank you so much, Charles.

Your reply is really helpful. I also wanted to ask that if I want to estimate the difference within these five numbers (instead of their normal distribution) to find whether the difference is at a significant level, what kind of statistical test is suitable?

Thanks again.

Sorry, I did not make it clear.

These five numbers are means of five groups. I wanted to compare these five means to find whether data from these groups are significantly different.

Stacey,

You can use ANOVA. The input will be raw data for each group, not the means.

Charles

Thanks a lot. I wanna say your suggestion is really helpful. It is so kind.

I’ve read your introduction for an ANOVA test. Pardon me for another question. Five groups of raw data do not meet either the the normality assumption or homogeneity of variance test (their p value are all equal zero). However, the sample sizes are equal, with each group containing 5000 samples. Under this situation, an ANOVA test is OK?

Thanks a lot!

Thanks Charles.

Since the null hypothesis for KS is that they are not normally distributed, which means they are significantly different from each other. If I just want to compare several figures, for example, 1.31, 1.24, 1.56, 1.67, 1.45, to find out whether they are significantly different from each other, only an one-sample KS test is OK?

Hi,

I am trying to figure out how to use the K-S Test to evaluate the plausible randomness (or lack thereof) of a binary Heads-Tails sequence with n=200. It seems this should be possible with a minor tweak to what you present in these pages. Could you point me in the right direction?

Thanks,

Robert

Robert,

As described on the referenced webpage, the KS test can be used to determine whether a sample fits a particular distribution. For the case you have identified this distribution is a uniform distribution with endpoints 0 and 1.

Charles

Before doing one way ANOVA test, should we check the nomarlity of the population where the data were collected from by one sample KS, or check the normality of the the data itself by KS? In brief, should we do one sample KS or KS before we do one way ANOVA test???

Thanks for your reply. This question has bothered me for quite a long time.

The answer is yes. You should check normality before doing an ANOVA. However, note that ANOVA is pretty robust to violations of normality, provided the data is reasonably symmetric and the group samples are equal in size.

I provide a number of tests for normality on the website, and so I suggest you take a look at the webpage Testing for Normality and Symmetry. In particular, I would use either the Lilliefors test (which is related to the KS test) or the Shapiro-Wilk test for normality.

Charles

Thanks Charles

I spend a few hours to get Real Statistics Resource Pack to work on Excel 2007 dutch version

Hi Charles,

Nice article

I can’t find the function =KSCRIT(B21,0.05) in Excel.

I am using Excel 2007

Greetings

Afke

Afke,

KSCRIT is not a standard Excel function. You need to install the Real Statistics Resource Pack to use it.

Charles

Hi sir , why is two table for critical value of D (k-s test) , that in one table (α=0.05) and (n=25) ———–> D = 0.180 and in other table (α=0.05) and (n=25) D = 0.264 ????!!!!

for k-s test Normality i use this table ———–>

https://real-statistics.com/statistics-tables/kolmogorov-smirnov-table/

or this table ———–>

http://lya.fciencias.unam.mx/rfuentes/K-S_Lilliefors.pdf

thank you

excuse me for bad English

Hi Masoud,

The article that you reference explains that the table of critical values for KS are too high when the test is restricted to just the normal distribution. In fact for low values of n the values the authors calculated specifically for the normal distribution are about 2/3 of the general table values, which is consistent with .180 and .264. The table of critical values given in the Real Statistics website are for the general KS test.

This article seems to imply that if you want to use KS you should use critical values that are specifically calculated for the distribution you want to test (normal, uniform, exponential, etc.). In the case of the normal distribution I generally use the Shapiro-Wilk test which gives better results, and so I avoid this issue.

Charles

Hi Charles,

I’m a little confused about the KS table here. You chose α = .05 in this case, does it mean that there’s 95% chance that the distribution is not different from the expected distribution (exponential distribution in this case)? But why Dn,α goes smaller as the α increases? For example, in my case, D = 0.123 and n = 150. If I choose α = 0.05, Dn,α = 0.111 and I have to reject the null hypothesis, but if I choose α = 0.01, Dn,α = 0.133 and I can say my distribution is the same as expected. So what does α actually mean here and how should I choose it?

Thanks a lot!!

Chen

Chen,

The null hypothesis is that the two distributions are equal. The value of alpha is as described in Hypothesis Testing. Generally alpha is chosen to be .05, but you may choose a different value, based on how much error you can tolerate.

Charles

Hi

I have taken 22 different(softwares) samples of 2 different variables and first one contains 4 independent variables and second one contains 7 independent variables.In this situation can we apply ks test or which test can be applied in this situation?

Hi,

You need to specify what you are trying to test, before I can tell you which test to use.

If you are trying to compare two samples with different variables, then I would have to respond that this is like comparing apples with oranges.

Charles